Uber Stock Analysis: Strong Revenue Growth, But Guidance Gives Pause

Uber Technologies, Inc. (NYSE: UBER) delivered a powerful third quarter in 2025, the results released on November 04, 2025, demonstrating significant growth across its core segments that confirms its status as an established mobility and delivery leader.

Q3 2025 Performance

The core business metrics were impressive:

Accelerating Growth: Trips soared 22% year-over-year to $3.5 billion, driven by a 17% increase in Monthly Active Platform Consumers (MAPCs) and 4% growth in monthly trips per MAPC. Total gross bookings grew 21% year-over-year to $49.7 billion. This impressive performance was driven by:

- Mobility: Gross bookings rose 20% year-over-year to $25.1 billion.

- Delivery: Gross bookings accelerated 25% year-over-year to $23.3 billion, underscoring robust consumer demand.

Revenue Growth: Total revenue for the quarter grew 20% year-over-year to $13.5 billion. Mobility revenue grew 20% year-over-year to $7.7 billion. Delivery segment saw its revenue rocket 29% year-over-year to $4.5 billion.

Profitability & Cash Flow: Adjusted EBITDA expanded 33% year-over-year to $2.3 billion, and the company generated strong Free Cash Flow of $2.2 billion. Management is focused on returning capital and redeeming its $1.2 billion Convertible Notes in Q4 2025.

CEO Dara Khosrowshahi emphasized a commitment to "investing in lifelong customer relationships, leaning into our local commerce strategy, and harnessing the transformative potential of AI and autonomy."

The Market's Reaction

Despite the stellar Q3 numbers, the stock experienced selling pressure immediately following the report.

The primary points of investor caution include:

Q4 EBITDA Guidance: The forecast for Q4 Adjusted EBITDA, while representing 31% to 36% year-over-year growth ($2.41 billion to $2.51 billion), was perceived by analysts as a downbeat earnings forecast for the key holiday quarter, according to Reuters.

Income from Operations: Revenue for the period reached $13.5 billion, marking a strong 20% increase year-over-year. However, income from operations told a different story. The income from operations figure stood at $1.1 billion, representing a modest 5% growth compared to the same quarter last year. More importantly, this figure reveals a sequential dip. Compared to the $1.5 billion in income from operations reported in Q2 2025, the latest quarter’s operational income is down $0.4 billion. raising questions about the pace of near-term margin expansion.

Freight Stagnation: The freight segment remained flat year-over-year in both gross bookings and revenue, signaling that this division has stabilized but is not yet contributing to overall growth momentum.

Uber Deepens NVIDIA Partnership for Autonomous Fleet Expansion

The most significant long-term vision introduced during this period is Uber’s deepened commitment to autonomous mobility, solidified by its major partnership with NVIDIA and Stellantis, announced on October 28, 2025.

Uber is leveraging the cutting-edge NVIDIA DRIVE AGX Hyperion 10 platform, which includes the safety-certified NVIDIA DriveOS and full-stack DRIVE AV software, to accelerate the rollout of Level 4 (L4) autonomous fleets. This commitment is underpinned by Stellantis, which will be among the first OEMs to deliver at least 5,000 L4 vehicles specifically for Uber’s robotaxi operations in the United States and internationally.

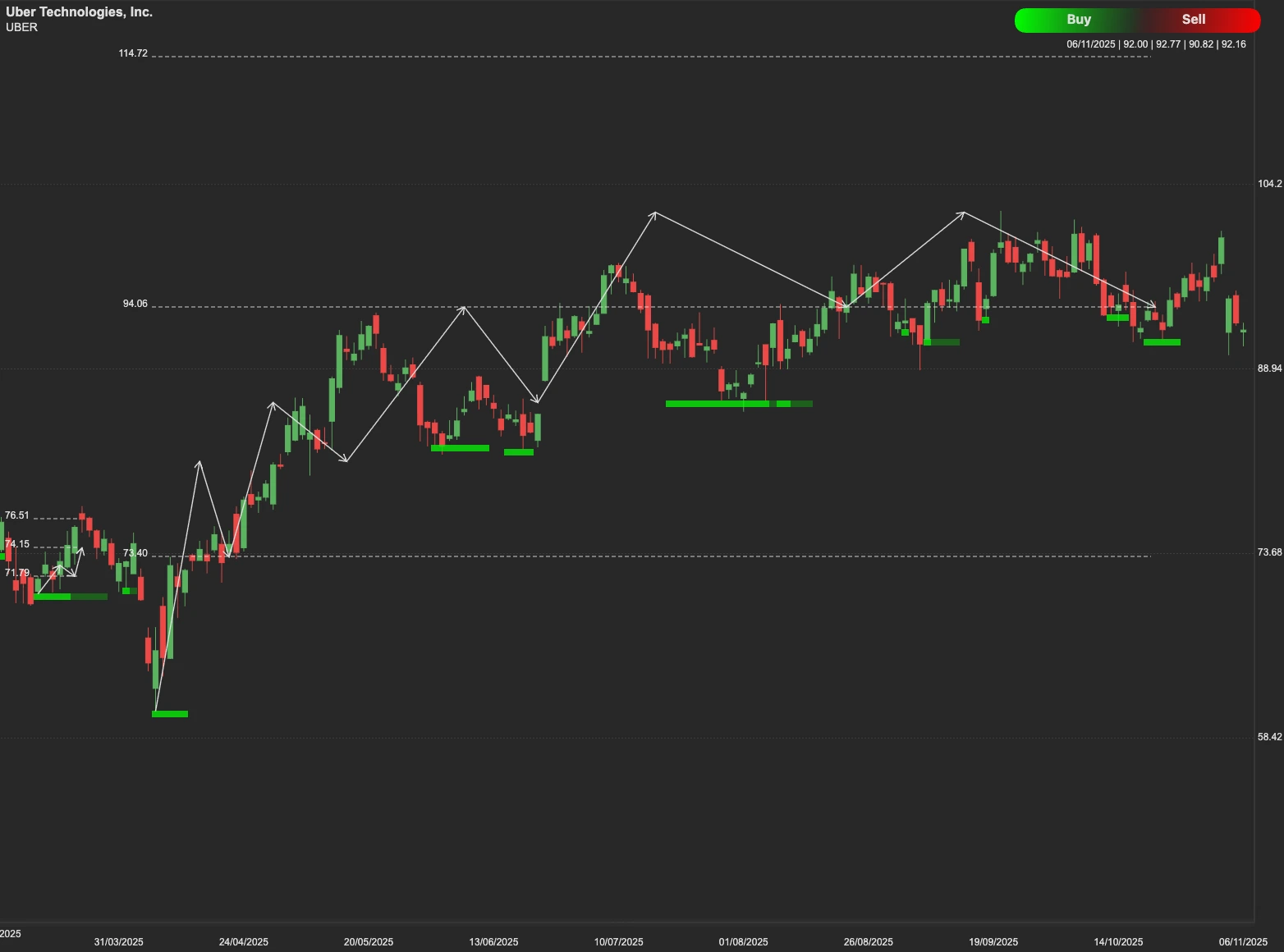

Technical Outlook

From a technical perspective, the $102 level represents the major immediate overhead resistance. Should the stock successfully sustain a move above the $102 resistance, the next primary price target is $110. However, if the stock fails to regain momentum and is rejected at the $102 ceiling, a downward move would seek the nearest key support level at $80. A failure to hold $80 would signal a deeper correction. Should selling pressure continue, the stock could seek the further support range between $75 and $66.